Authors: David Duong, CFA (Head of Research) and Colin Basco (Research Associate) |

Market looks past the shutdown |

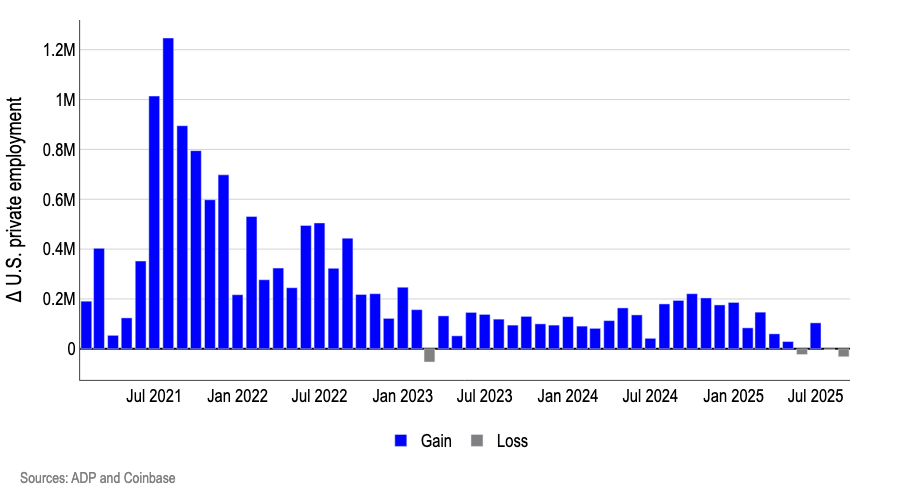

Our October outlook is tactically bullish: we think US dollar softness, a short-term global liquidity impulse, and a Fed policy bias toward insurance cuts create a favorable market setup for crypto. Absent a hawkish surprise, we think these conditions increase the odds of BTC-led upside until November where liquidity headwinds may come into play. What does the US government shutdown mean for crypto? The US is now in a partial government shutdown, which could delay the release of some key economic statistics that the Fed relies on for their policy decisions. Because of funding lapses, agencies such as the Bureau of Labor Statistics (BLS) and Bureau of Economic Analysis (BEA) will suspend data collection and delay major releases—including the monthly jobs report and CPI—until funding is restored. Absent official data releases, we think markets will lean on private gauges like ADP private employment to price expectations of future rate cuts. ADP now shows essentially zero net job creation at the margin after a multi-year deceleration from 2021’s million-plus monthly gains (Chart 1). In our view, Phillips-curve logic implies that softer hiring today narrows the pipeline to wage-led services inflation on ~10 month lag, which reduces the cost of easing preemptively relative to the tail-risk of a nonlinear labor downturn. Our view: Shutdown-driven data uncertainty plus a stall in private hiring raises optimism for a less restrictive Fed policy path. Note too that a confluence of factors recently led to a temporary liquidity vacuum in crypto markets, including (1) the US Treasury rebuild of its general account balance (now near target at over $800B), (2) quarter-end / month-end flows and (3) the conference effect of Token2049 in Singapore. The lifting of these effects should help price dynamics in the short term. |

Chart 1. Monthly change in U.S. private employment at lowest level since 2023 |

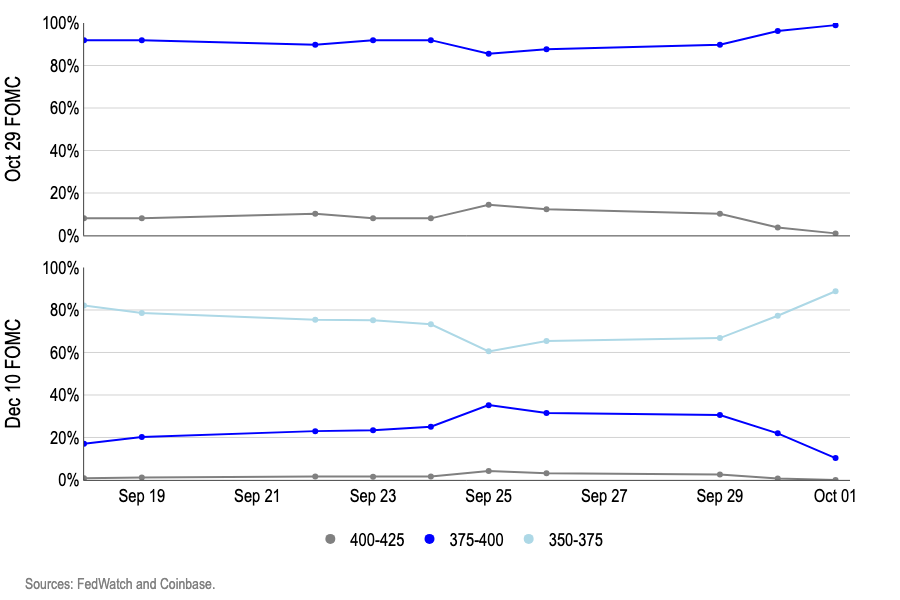

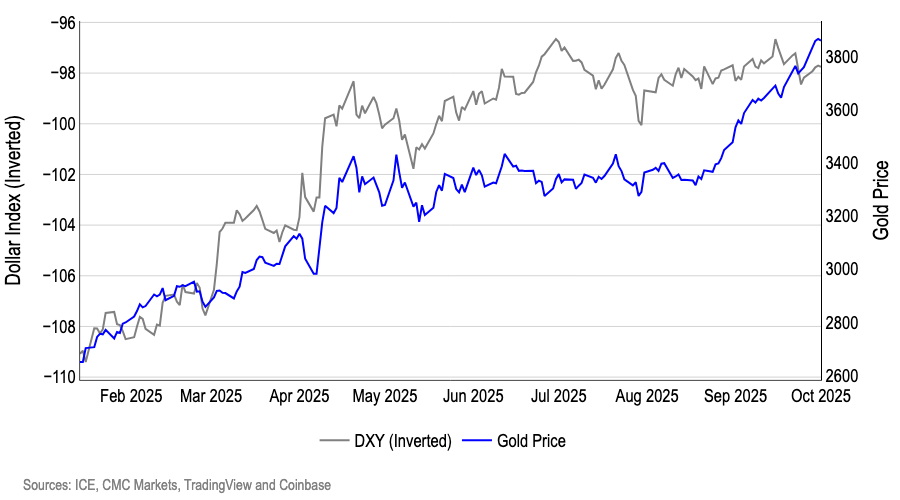

We think rate markets have already priced in that shift—30 day Fed fund futures now price in an 87% chance of two 25bps cuts by year-end—and cross-asset signals validate a lower real-rate, dollar-softer regime that is supportive for crypto (Chart 2). Meeting-by-meeting pricing now concentrates in the 3.75–4.00% target range for late October and drifts toward 3.50–3.75% by December, while the dollar weakens alongside gold hitting new all time highs—a sign of easing real-rate expectations and a broader “store-of-value” bid (Chart 3). In our view, this combination loosens USD financial conditions and reduces cash-yield competition for risk assets, which should benefit crypto. |

Chart 2. Odds of two 25bp cuts by year-end reach 87%. |

Chart 3. Dollar softens while gold hits new all time highs |

Can we stop talking about gold? |

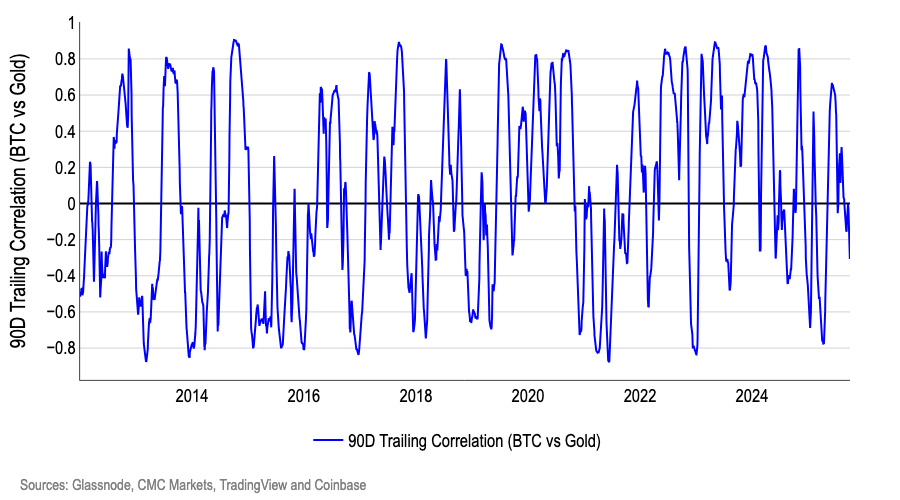

The short answer is no, but the market seems to be at pains to explain why gold breached new all-time-highs in September while bitcoin’s price action languished last month. Part of that is because many market players and media pundits remain fixated on the idea of bitcoin as an inflation hedge akin to gold, despite the latter’s inconsistent performance during high inflation periods. The reality is that bitcoin tends to function as protection against excess money creation, which isn’t quite the same as inflation. This also explains why bitcoin often benefits from global liquidity injections. Gold surged in September on the back of rate cuts from several global central banks as well as concerns about (1) the US government shutdown and (2) Fed independence potentially being compromised. (That said, while the SPDR Gold ETF attracted $4.2B last month, US spot bitcoin ETFs still gained a comparable $3.5B in net inflows.) However, we think the performance disparity was less about divergent institutional sentiment and more about bitcoin front running the price action in July and August. Consequently, bitcoin exhibited consistent sell pressure on technical bounces, while liquidity was being sucked out of the system for the aforementioned reasons. From a data perspective, we think gold alone isn’t a strong indicator for bitcoin. The 90-day rolling correlation between BTC and gold has swung from both extremes (−0.8 to +0.8) dozens of times since 2013, with short clustering but no long-run persistence, indicating that average co-movement is extremely weak (Chart 4). In our view, the common driver behind episodes of positive co-movement is higher liquidity: when real rates fall and the dollar softens, both assets tend to soak up excess liquidity in the market. Conversely, when gold rallies on flight-to-quality while the dollar strengthens and liquidity tightens (as it has in recent weeks), BTC often decouples or even moves the other way as a higher-beta risk asset. Our view: Practically, we think liquidity is the most reliable macro signal for bitcoin as proven by consistent ~0.9 correlations of our custom M2 global liquidity index with bitcoin over the past three years. |

Chart 4. Trailing 90 day correlation of Bitcoin versus Gold |

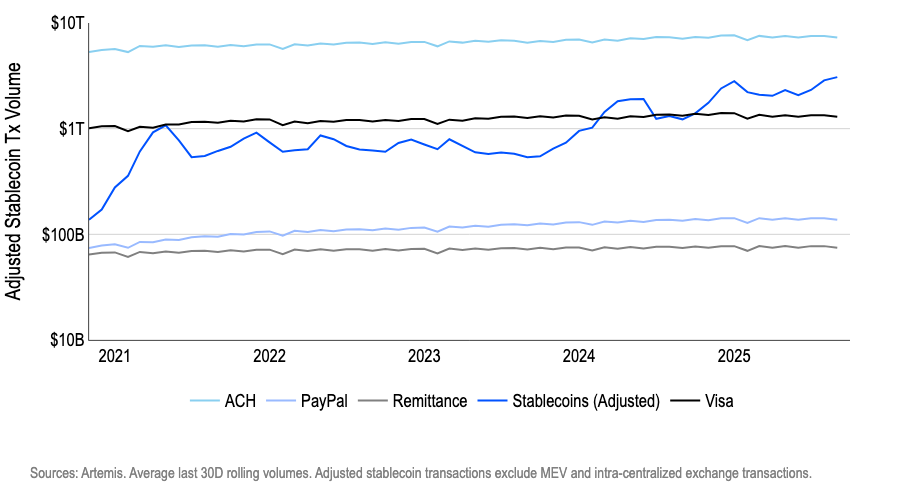

The decision by SWIFT (a secure messaging platform for international financial transactions) to add a blockchain-based shared ledger formally mainstreams the digital economy by enabling bank-grade settlement for stablecoins and tokenized funds. Note that while this represents a watershed moment for both crypto and global finance, the announcement has been nearly eight years in the making. SWIFT has been working on digital ledger applications since 2017 and has made significant breakthroughs over the last two years. On September 29, SWIFT announced that it will embed a shared blockchain ledger into its infrastructure and is working with major banks and Consensys to frame a path for cross-border transactions that include stablecoins. This institutional catalyst lands as adjusted stablecoin transaction volume rose ~7% M/M to reach $3.07T in September, well above major retail payment rails (Chart 5). In light of these developments, we think our stablecoin projections of reaching a $1.2T market cap by 2028 appear even more reasonable. Our view: SWIFT’s move materially lowers the integration cost for financial institutions to route stablecoin payments across networks. |

Chart 5. Adjusted stablecoin transaction volumes surpass $3T in September |

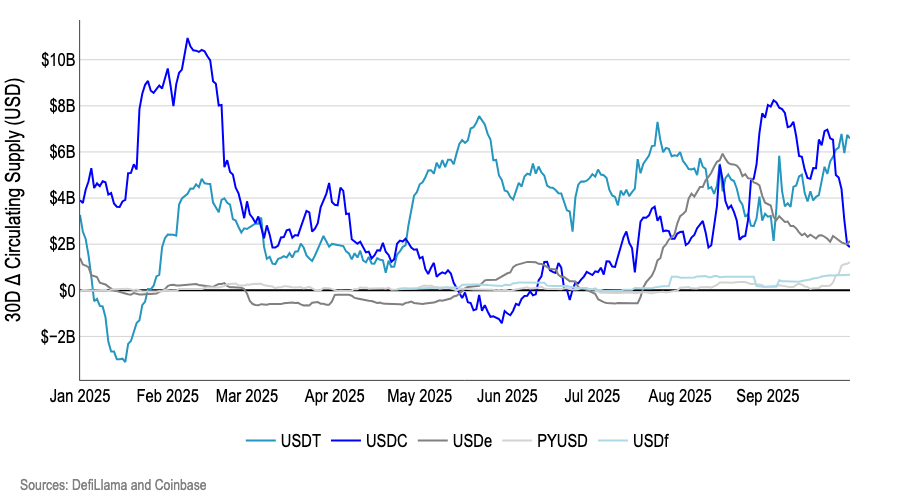

Tether is reportedly seeking between $15-20B in fresh capital in exchange for ~3% of the company (via private placement) potentially valuing the stablecoin issuer at $500B. USDT currently retains a dominant 58% share of the stablecoin market, reinforced by Tether’s strategic ~$1B BTC purchase at the end of 3Q25 (as part of its strategy to allocate part of its profits to BTC accumulation). In our view, USDT’s outsized 30-day supply gain is being driven primarily by a surge in perpetual futures activity that predominantly quotes and margins in USDT (Chart 6). As aggregate perp open interest and volumes climb, traders source additional USDT for margin and for USDT-quoted spot legs; that mechanically pulls more USDT into circulation. The effect is amplified because most major CEXs default to USDT pairs (e.g., Binance, Bybit, OKX) in addition to popular new decentralized exchanges (DEXs) like Aster, which did 8x the volume of HyperLiquid in one day. Our view: As we discussed in last week’s commentary, we expect token speculation to continue being one of the primary use cases for crypto based on trends of surging DEX volumes despite compressing TVL growth. In this context of rising interest in leverage trading and token speculation, we think USDT will continue to benefit. |

Chart 6. Top stablecoins by 30-day change in market cap |

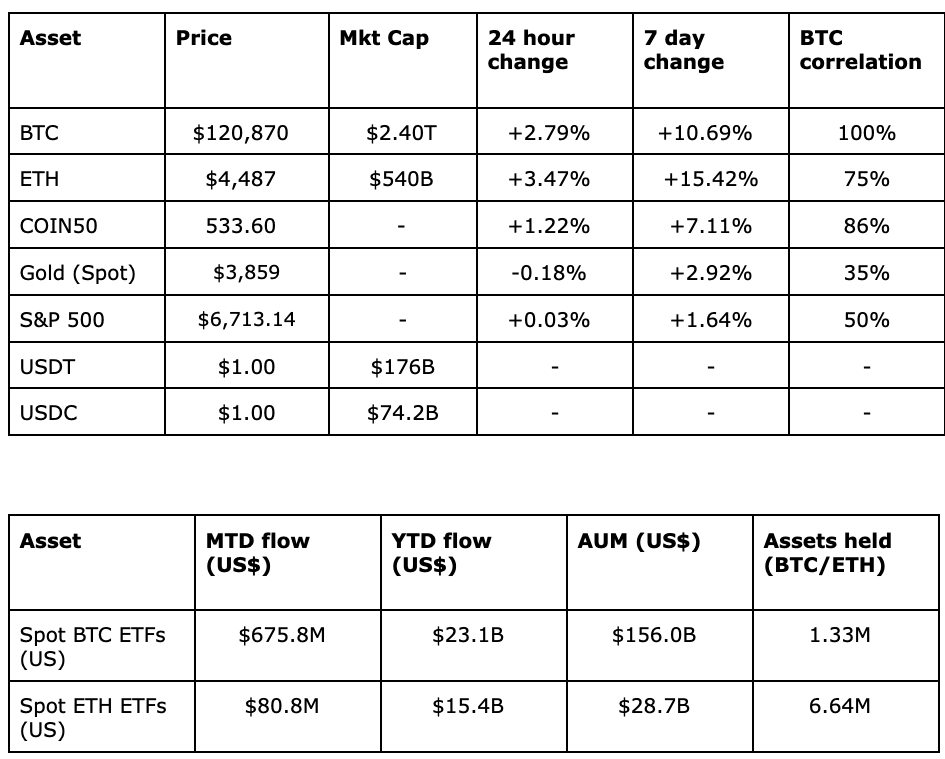

Crypto & Traditional Overview |

(Prices as of 4pm EDT, Oct 2 and ETF flows as of 4pm EDT, Oct 1 ) |

Source: Bloomberg and TradingView |

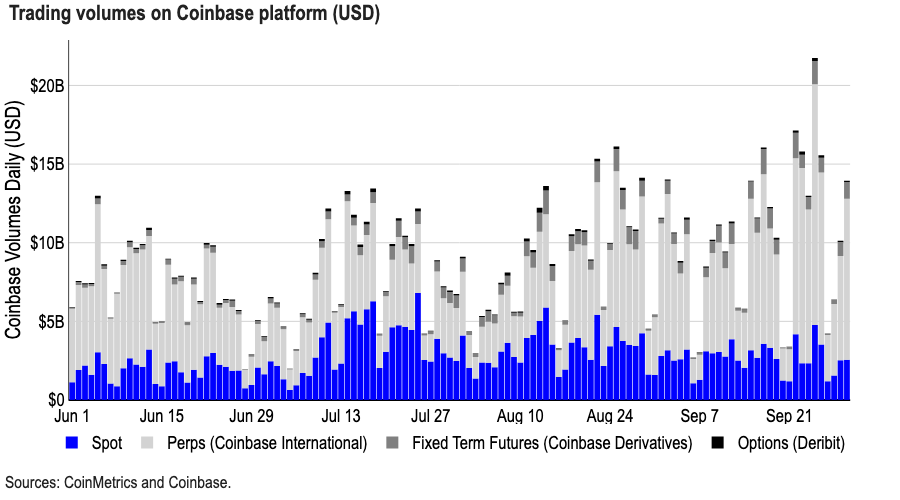

Coinbase Exchange & CES Insights |

Last week's drawdown reset positioning and created a solid foundation for the recent move higher in price. Leveraged traders have added long exposure in BTC and various altcoins such as SUI, XRP, and DOGE. However, funding rates for ETH and SOL still remain muted, suggesting light long positioning and a cautious approach from traders. Likewise, the options market is showing a similar divergence. The 1M 25D put-call option skew has gotten more bullish for BTC while staying relatively unchanged for ETH and SOL. |

For an archive of the weekly market commentary and all our other research reports, please visit our Research Portal. |

|

|

View replays of our weekly crypto market analyses from our Americas, APAC and EMEA Coinbase Institutional teams. |

| Not subscribed to the Weekly Market Commentary and want to be added to the list? |

|

|

| 2025 © Coinbase, Inc. All Rights Reserved. COINBASE and related logos are trademarks of Coinbase, Inc., or its Affiliates. The views and opinions expressed herein are those of the author(s) and do not necessarily reflect the views of Coinbase and summarizes information and articles with respect to cryptocurrencies or related topics. This material is for informational purposes only and is only intended for sophisticated investors, and is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of Coinbase. No representation or warranty is made, expressed or implied, with respect to the accuracy or completeness of the information or to the future performance of any digital asset, financial instrument or other market or economic measure. The information is believed to be current as of the date indicated and may not be updated or otherwise revised to reflect information that subsequently became available or a change in circumstances after the date of publication. Coinbase, its affiliates and its employees do not make any representation or warranty, expressed or implied, as to accuracy or completeness of the information or any other information transmitted or made available. Certain statements in this document provide predictions and there is no guarantee that such predictions are currently accurate or will ultimately be realized. Prior results that are presented here are not guaranteed and prior results do not guarantee future performance. Recipients should consult their advisors before making any investment decision. Coinbase may have financial interests in, or relationships with, some of the assets, entities and/or publications discussed or otherwise referenced in the materials. Certain links that may be provided in the materials are provided for convenience and do not imply Coinbase’s endorsement, or approval of any third-party websites or their content. Any use, review, retransmission, distribution, or reproduction of these materials, in whole or in part, is strictly prohibited in any form without the express written approval of Coinbase. To the extent you make use of trading services, these may be provided to you by Coinbase, Inc. or Coinbase Luxembourg S.A. (“CB Lux”), subject to applicable law and depending on your location. Coinbase, Inc. is licensed to engage in virtual currency business activity by the New York State Department of Financial Services. Coinbase, Inc., 248 3rd St #434, Oakland, CA 94607. CB Lux is authorised by the Luxembourg Commission de Surveillance du Secteur Financier to provide certain crypto-asset services pursuant to the European Union’s ‘Markets in Crypto-Assets’ regulation. | © Coinbase 2025 | Coinbase Custody International Limited

70 Sir John Rogerson’s Quay | Dublin 2 | D02 R296 | Ireland

www.coinbase.com

Get in touch

In the UK, this communication is directed only at persons who are investment professionals for the purposes of the Financial Services and Markets Act 2000 (Financial Promotion) 2001, as amended, having professional experience relating to investments. Any mentioned products and services are only available to such persons.

Any person who is not an investment professional should not rely on this communication.

For these purposes, an investment professional includes:

1. an authorised person;

2. any other person whose ordinary activities involve him in carrying on the cryptoasset trading activity by way of business; or

3. a government, local authority (whether in the United Kingdom or elsewhere) or an international organisation

Unsubscribe from future editions of this type of message. | | | |

|

|

|